A no deal Brexit will put the boot in for Japanese companies in the UK

My first job at Mitsubishi Corporation was exporting British made shoes from companies like Trickers and Crockett & Jones to Japan. They are high end shoes anyway, and Japanese tariffs of 30% on shoe imports certainly pushed them even further upmarket. So when I was in Japan last month I was happy to see that one of our customers still had its Trading Post flagship shop in Aoyama, despite the so-called two lost decades in terms of economic growth. They must be one of the few businesses enjoying the fact that Brexit delays have improved their profit margins. Thanks to the new EU-Japan Economic Partnership Agreement, tariffs on European shoe exports to Japan were reduced to 21% from February of this year. They will eventually be eliminated over the next 10 years.

Trickers and Crockett & Jones are presumably shipping out shoes to Japan as fast as they can make them while the UK’s membership of the EU lasts. Although Japan has entered discussions with the UK on a trade deal, they have made it clear that they are not going to concede as much as they did to the EU, and leather goods is one of the categories they are going to use as a bargaining weapon.

No roll over is bad for British shoes, cheese and booze

So a no deal Brexit or a Brexit before a UK-Japan free trade agreement is struck is bad news for the UK shoe industry, (and British cheese makers and whisky distillers will also miss out on the EPA’s tariff reductions). But not rolling over the EU-Japan EPA in to a UK-Japan trade agreement as soon as the UK leaves the EU will only have a small direct impact on both economies. According to a JETRO survey of over 3,000 Japanese companies, from March of this year, only 8.6% import from the UK, compared to 24.1% importing from Western Europe (excluding the UK) 66.2% from China and 24.2% from the USA.

Conversely, 22% of Japanese companies export to the UK, compared to 35% exporting to non-UK Western Europe, 49.6% to the USA and 59% to China. It’s obvious from these figures why the US-China trade war is more concerning to Japan than Brexit.

You could argue that a UK-Japan free trade agreement would improve those percentages, but that’s an awful lot of shoes, cheese and booze to make any impact. Furthermore, a lot of the imports and exports between the UK and Japan may be EU related, rather than purely bilateral. Think car parts from Japan to build cars for European consumers, or UK generated professional services for a Japanese EU headquarters and its European subsidiaries.

But no deal with the EU is even more of a headache for Japanese companies in the UK

Japanese companies that have a presence in the UK (just under 10% of the companies surveyed) have made it very clear that a No (UK-EU) Deal Brexit would be a disaster for them – far more than the UK no longer being part of the EU-Japan EPA. As frequently pointed out, they invested in the UK as a gateway to the rest of Europe.

45% of the turnover of Japanese companies in the UK is sales to Europe according to figures from the annual reports of the 200 or so who give regional breakdowns of sales. The range is anywhere from close to 0% for companies selling everything from lighting to metal pressing to seeds just to the UK, through to 100% – largely automotive parts manufacturers who export almost all of their production to Europe, or at least sell it via their European headquarters in continental Europe.

Many of those who are focused on domestic UK sales are importing from Japan, China and Asia, or are at the end of a complex supply chain stretching across Europe. Some are not involved in trade of goods at all – for example NTT Data and Building Design Partnership. The latter is one of the many of the services sector companies that have recently become Japan-owned via acquisition. NTT is aiming to grow its UK government business after Brexit, but if the UK economy tanks thanks to a no deal, it may have to wait a while. A JETRO survey last year highlighted that a UK economic slump because of Brexit was at the top of the list of concerns for Japanese companies in the UK and the rest of the EU, even more than changes in regulation or currency fluctuations.

The UK looks to lose its crown as the top European destination for Japanese acquisitions

Japanese acquisitions of British companies continued after the referendum, but the 2019 JETRO survey shows that it is likely the UK will lose its crown as the top destination in the EU for Japanese foreign direct investment. Non-UK Western Europe is in the top five destinations for expanding business for manufacturing textiles, clothing, foods, petrochemicals/plastics, electrical machinery, electronic components, fine engineering and also specialist services. The UK does not feature at all in the top five of any of these sectors.

The UK’s service sector functions as a gateway to Europe is still the biggest influence on Japanese investment – the UK is a top 20 destination for expanding services such as regional coordination(#9), logistics (#13), R&D (#14), sales (#15) and localisation (#17), as well as high value added manufacturing (#17). However, non-UK Western Europe ranks higher and is in the top 10 destinations for all of these categories.

For more content like this, subscribe to the free Rudlin Consulting Newsletter. 最新の在欧日系企業の状況については無料の月刊Rudlin Consulting ニューズレターにご登録ください。

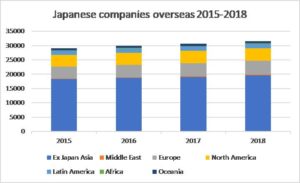

Growth in the number of Japanese companies overseas has been more muted in the past 4 years – a 7.9% increase 2015-2018. But the increase in the number of Japanese companies in Europe was above average – at 12.5%. The increases in companies in Asia (7.6%) and Latin America (5.6%) were below average – so there was a boom in Japanese investment in developing countries during the 2008-2014 period, but this died down in the past 4 years.

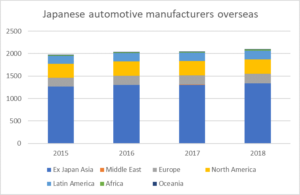

Growth in the number of Japanese companies overseas has been more muted in the past 4 years – a 7.9% increase 2015-2018. But the increase in the number of Japanese companies in Europe was above average – at 12.5%. The increases in companies in Asia (7.6%) and Latin America (5.6%) were below average – so there was a boom in Japanese investment in developing countries during the 2008-2014 period, but this died down in the past 4 years. So how about investment in automotive manufacturing – the sector that has made the most noise in Brexit UK? The number of Japanese companies overseas in the “transportation machinery manufacturing” category that Toyo Keizai uses (which presumably corresponds to automotive manufacturing) rose 6% 2015-2018, so significantly slower growth than overall. Again, Europe showed above average growth of 13%, but only represents 10% of transportation machinery manufacturers overseas operations. Over 64% of automotive manufacturer sites are in ex-Japan Asia. So although Japanese automotive companies are not pulling out of Europe – rather the reverse – the major part of Japanese automotive investment is and continues to be in Asia. So no surprises really that Honda and others are choosing to focus on Asia for electric vehicle development – that is where the largest ecosystems and supply chains are based.

So how about investment in automotive manufacturing – the sector that has made the most noise in Brexit UK? The number of Japanese companies overseas in the “transportation machinery manufacturing” category that Toyo Keizai uses (which presumably corresponds to automotive manufacturing) rose 6% 2015-2018, so significantly slower growth than overall. Again, Europe showed above average growth of 13%, but only represents 10% of transportation machinery manufacturers overseas operations. Over 64% of automotive manufacturer sites are in ex-Japan Asia. So although Japanese automotive companies are not pulling out of Europe – rather the reverse – the major part of Japanese automotive investment is and continues to be in Asia. So no surprises really that Honda and others are choosing to focus on Asia for electric vehicle development – that is where the largest ecosystems and supply chains are based. UK is the birthplace of innovation and will not sink, despite Brexit,

UK is the birthplace of innovation and will not sink, despite Brexit, Japanese companies used to be seen as very reluctant to acquire and merge with other companies, but the record breaking £46bn acquisition, finalised in January 2019, of Irish pharmaceuticals company Shire by Japan’s Takeda may not even be the peak of what has been at least 10 years’ of an overseas spending spree by Japanese companies. Faced with a declining, ageing domestic market,

Japanese companies used to be seen as very reluctant to acquire and merge with other companies, but the record breaking £46bn acquisition, finalised in January 2019, of Irish pharmaceuticals company Shire by Japan’s Takeda may not even be the peak of what has been at least 10 years’ of an overseas spending spree by Japanese companies. Faced with a declining, ageing domestic market,  Although around 10,000 manufacturing jobs in Japanese electronics companies in the UK were lost in the 1990s-2000s, about the same number have been added, either created by Hitachi Rail or in the automotive or air conditioning sectors. Japanese electronics companies such as Sony, Fujitsu, Panasonic, NEC, Mitsubishi Electric and Hitachi still all employ thousands of people in the UK.

Although around 10,000 manufacturing jobs in Japanese electronics companies in the UK were lost in the 1990s-2000s, about the same number have been added, either created by Hitachi Rail or in the automotive or air conditioning sectors. Japanese electronics companies such as Sony, Fujitsu, Panasonic, NEC, Mitsubishi Electric and Hitachi still all employ thousands of people in the UK.