What do the trends in Japanese residents overseas tell us about Japan’s relations with the UK and the rest of the world?

Headline findings

- The headline number for Japanese nationals in the UK is deceptively stable concealing a rise in permanent residents, overtaking those on long term visas as the majority

- The UK has shifted from being a posting destination for corporate Japan and a place to study for Japanese students towards being a settlement destination for individual Japanese

- Brexit accelerated trends in the UK that were already there, globally, since the Global Financial Crisis of 2008-9

- The number of students who were Japanese nationals on degree courses in the UK of over a year declined due to financial issues, and the number of students who were Japanese nationals on shorter courses declined due to student visa regulations tightening

- The decline in Japanese corporate expatriation is explained by cost (exchange rate and visa costs), access to the EU market and growth prospects

Overview

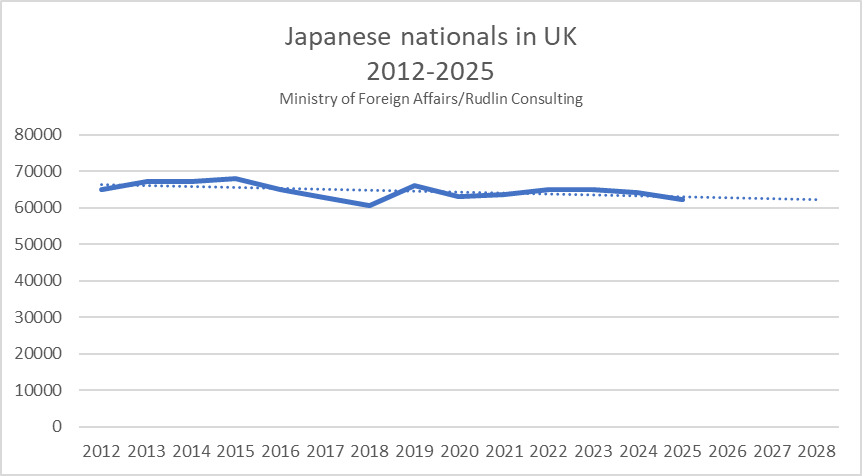

The headline number for Japanese nationals in the UK is deceptively stable: 63,011 Japanese nationals lived in the UK in 2011 and 62,270 in 2025. Underneath, the population has been transformed.

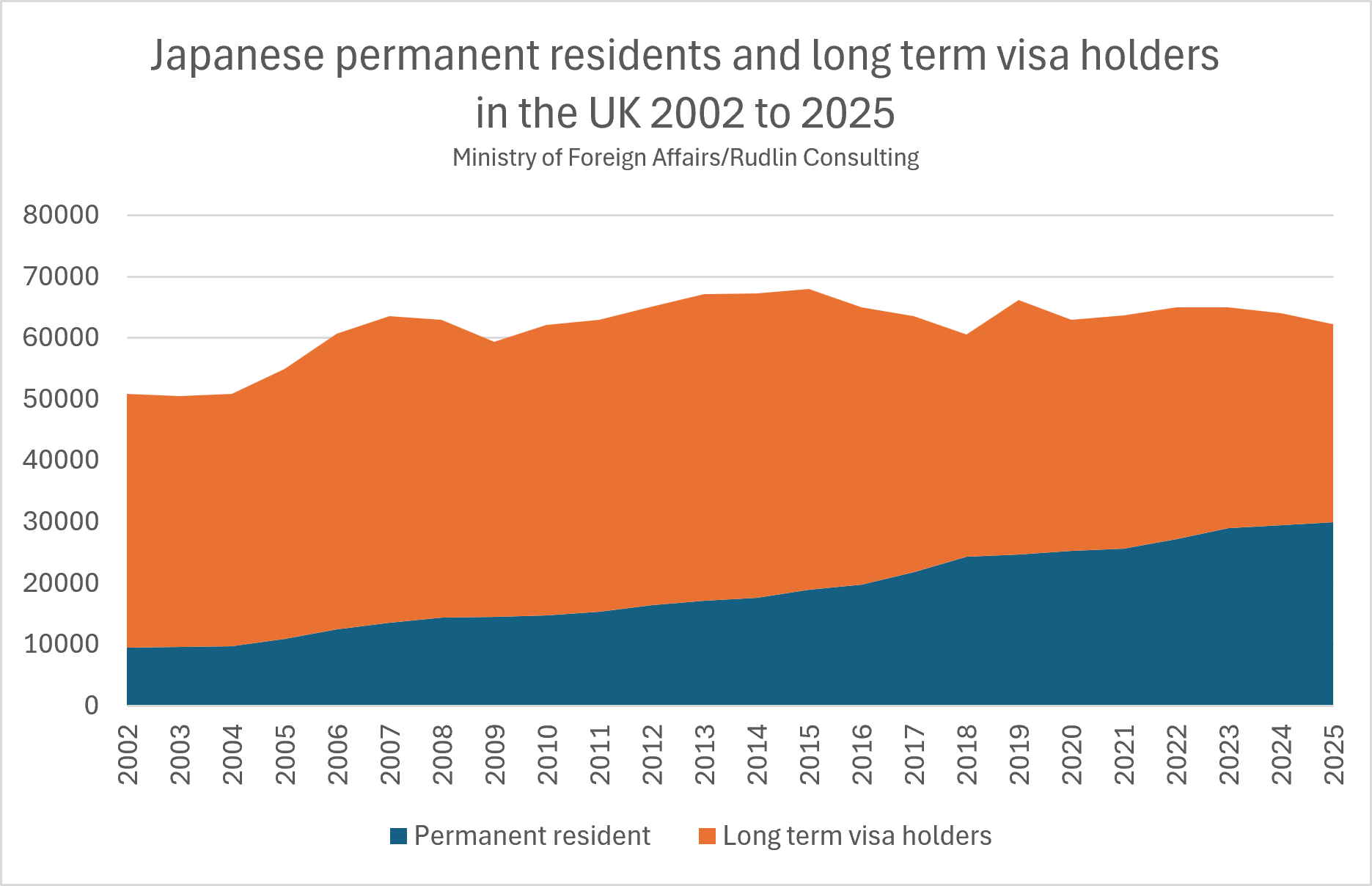

Long-term residents – the category that contains students enrolled in degree courses and corporate rotational staff and their families – peaked at 50,016 in 2013 and has fallen almost every year since the Brexit referendum, to 32,315 in 2025, a decline of 35% from the peak.

Permanent residents have moved in exactly the opposite direction, nearly doubling from 15,325 in 2011 to 29,955 in 2025. The UK has shifted from being a posting destination for corporate Japan and a place to study for Japanese students towards being a settlement destination for individual Japanese.

Between 2015 and 2018 – after the Brexit referendum was called, through the vote and the Article 50 uncertainty, but before COVID – UK long-term Japanese residents fell 25.9%, from 49,066 to 36,351. Over the same three years the equivalent population rose 3.5% in Germany, 8.7% in France, 31.8% in the Netherlands, 6.0% in Australia and was flat in the USA. The UK was the only major host country losing Japanese long-term residents in that window.

The UK continues to be the sixth largest host globally of Japanese nationals but the Japanese population in other large host countries such as Australia, Canada and Germany has grown by double figures over the same period. Overall, the number of Japanese living overseas has declined by only 1.4% from 2015-2025.

Is Brexit the cause of Japanese nationals working or studying elsewhere? As we shall see, Brexit accelerated trends that were already there. The UK government was trying to restrain the number of foreign students coming to the UK even before the referendum, as a means to reduce total immigration numbers. These new restrictions undoubtedly impacted Japanese students, along with a weak yen in 2014-5.

The repeat of a weakening yen since 2021 and the rising expense and stricter criteria for working visas, added to the reduced attraction of investing in a post-Brexit UK as a gateway to the EU. This has undoubtedly caused the further decline in corporate long term visa holders.

Something impacted the UK more than the rest of the world 2015-2019

The total number of Japanese nationals in the UK shows a slow, bumpy decline of around 9% over the past 10 years. There was growth from 2012 to a peak of 68,000 in 2015, falling to just over 62,000 in 2025. There was some recovery around 2019 and again after the pandemic, but not back to previous levels.

Figure 1. Japanese nationals in the UK, 2012–2025 (total, with trend line). Source: Ministry of Foreign Affairs / Rudlin Consulting.

Looking at the global picture, there are some similar patterns to the UK, suggesting that there are global or at least Japanese domestic trends at play – such as its shrinking, ageing population and the weakening yen. The total of Japanese nationals living overseas grew every year to a peak in 2019 of 1.4 million, and then declined to 2024, only slightly recovering in 2025, to 1.3 million. This represented an 8% decline from 2019 to 2025, but only a 1.4% decline 2015-2025, compared to -9% in the UK over the same 2015-25 period.

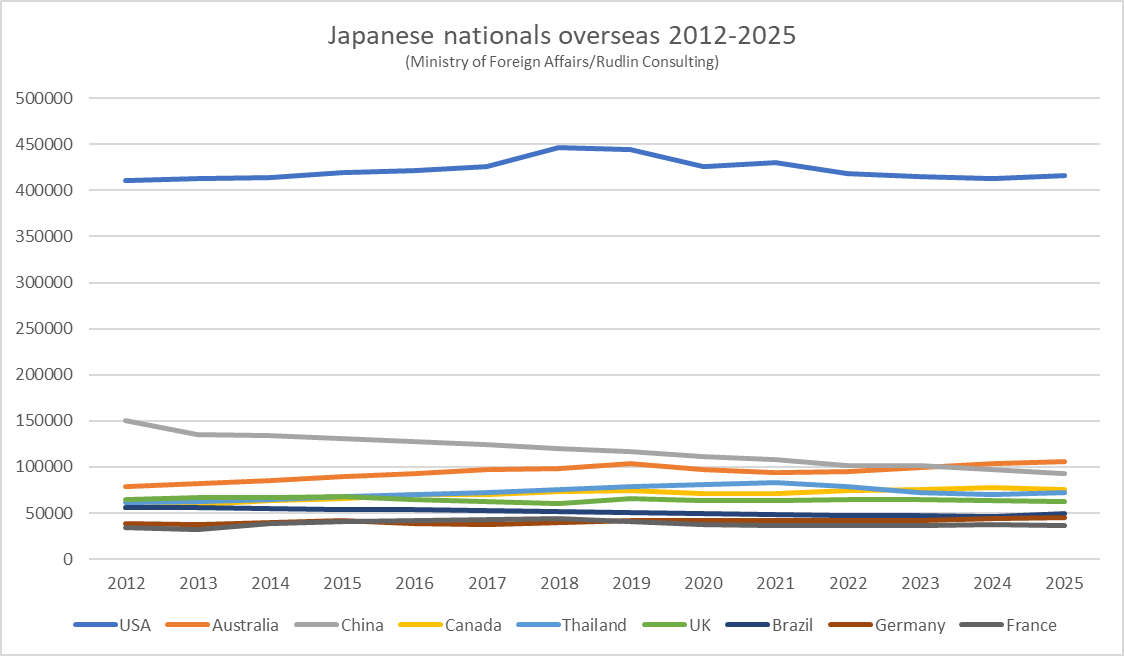

The UK continues to be the 6th biggest host of Japanese nationals worldwide, but the total number of 60,000 or so is dwarfed by the USA, which has over 416,000 Japanese nationals, a decline from a peak in 2018 of 447,000 – a trend which is very similar to the trends in overall global totals.

The other major contributor to the global decline since 2019 in Japanese nationals overseas is the significant drop in Japanese nationals living in China. This has been in steady decline since 2012.

The decline in Japanese resident in China may be a combination of two factors – a maturity after the initial China boom, when Japanese manufacturing invested heavily in setting up operations in China, and also a sign of the deteriorating relationship between China and Japan, starting from when Japanese businesses were targets of demonstrations in 2012, and Japanese people, including women and children, being attacked in Chinese cities as recently as this year.

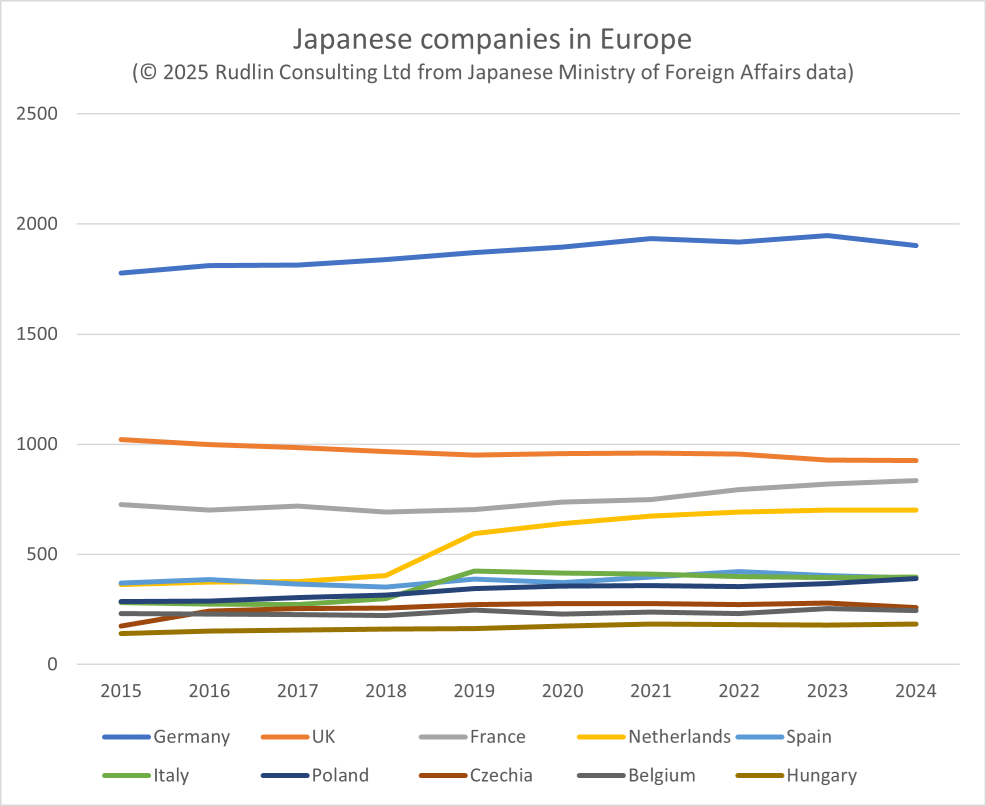

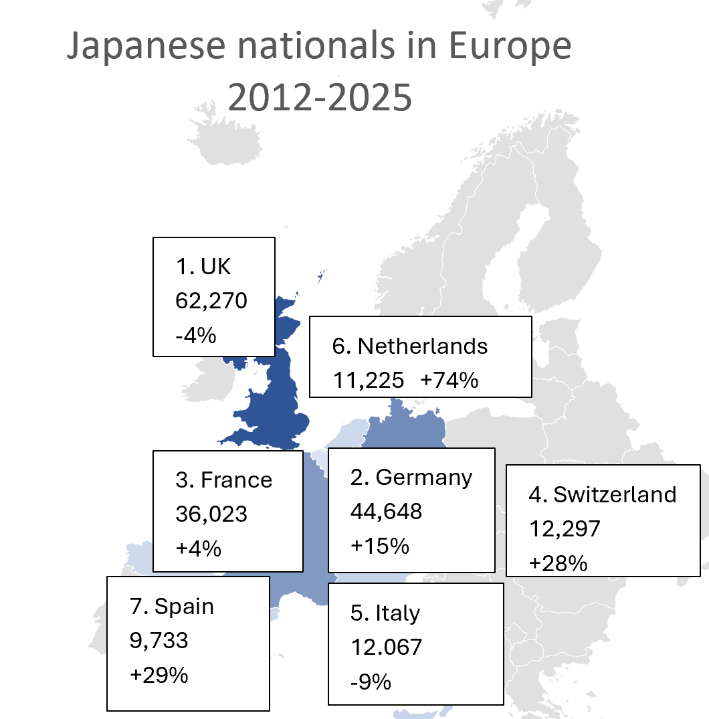

Figure 2. Japanese nationals in Europe, 2012–2025: leading host countries and their change over the period.

There has been consistent growth in resident Japanese nationals throughout the 2012-2025 period in Australia (+34%), Canada (+35%) and Germany (+15%).

Understanding why the UK has fared differently to fellow Anglophone countries such as the USA, Australia and Canada, and also other European countries such as Germany and France requires closer examination of the two major categories of residency.

Figure 3. Japanese nationals overseas, 2012–2025: the largest host countries.

Long term visa holders versus permanent residents

The two main categories used by Japan’s Ministry of Foreign Affairs for tracking Japanese nationals overseas are permanent resident and long term visa holder. Long-term visa holders mainly consist of corporate expatriates and students, academics and researchers and include anyone with a visa of 3 months or more in duration.

This latter category does not map directly onto UK visas, however. Academics coming to the UK to research, teach or attend conferences can get a standard visa of up to 12 months. Students coming for courses of under 6 months can enter the UK on a standard visitor visa, as can academics and researchers.

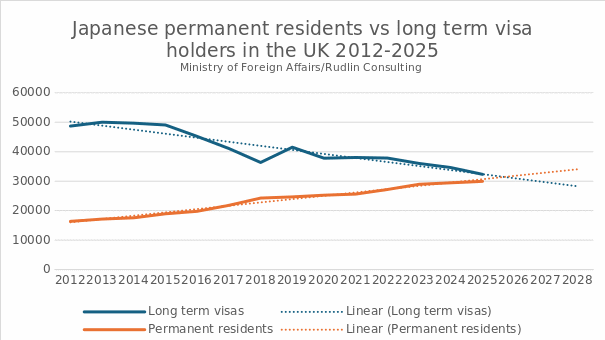

If we break down the total into these two categories, a strong trend emerges for Japanese nationals in the UK, which is that on current projections, the number of permanent residents will outstrip the number of long term visa holders in the near future.

Figure 4. Japanese permanent residents vs long-term visa holders in the UK, 2012–2025, with linear projections.

Looking back to 2002, it also becomes clear that the bumpiness in trends over the past twenty years are mostly due to changes in the numbers of long term visa holders, versus steady growth in permanent residents.

Figure 5. Japanese permanent residents and long-term visa holders in the UK, 2002–2025.

Again this reflects global trends for Japanese nationals – in 1991, 38% (251,000) of Japanese nationals overseas (663,000) were permanent residents. By 2025, 45% (588,000 – a record high) of Japanese nationals overseas were permanent residents.

Within Europe, the larger countries that now have more permanent resident than long term visa holding Japanese nationals are Sweden (since at least 1997), Switzerland (since 1999 ) and Italy (since 2023).

Globally, amongst the larger countries, Argentina, Australia, Brazil, Canada, New Zealand and the USA all have a majority of permanent residents amongst the Japanese nationals they host. This is partly down to historical factors – countries such as Brazil, Argentina and the USA were recipients of large numbers of migrants from Japan in the late nineteenth and early 20th centuries.

Many of the descendants of these migrants have retained their Japanese nationality and passports by birthright and only have permanent resident status in the country of their birth. Japan is one of the few countries in the world that does not allow dual nationality.

Conversely, the number of long term visa holders globally has declined from a peak in 2019 of 891,000 to 710,000 in 2025. This decline is apparent across all the major hosts of Japanese nationals, but the onset of the decline and the degree of recovery from the pandemic varies from country to country.

Long term visa holders are affected by exchange rate related expense, safety concerns and visa regulations.

For the USA there has been a 27% fall in the number of long term visa holders since 2012 and no signs of recovery since the pandemic.

For China, the fall is even more precipitous – 42% since 2012 , and the trend continued after the pandemic.

The number of long term visa holders in Thailand grew 27% overall since 2012, presumably as an alternative base to China, but has not grown since the 11% drop during the pandemic. Australia is the most positive story – growing 18% overall, and recovering since the pandemic with a 10% growth in long term visa holders over 2023-2025.

The decline in the number of long term visa holders in the UK is nearly as stark as China’s – an overall decline of 34% since 2012 including a 15% drop after the pandemic.

Why did the number of Japanese long term visa holders in the UK start to decline from 2015?

The number of long term visa holders in the UK held fairly steady from 2012 to 2015, at around 50,000. It then fell to 45,000 in 2016 and continued to fall to 2019, when there was a brief recovery, only to fall during the pandemic, with a continuing decline since.

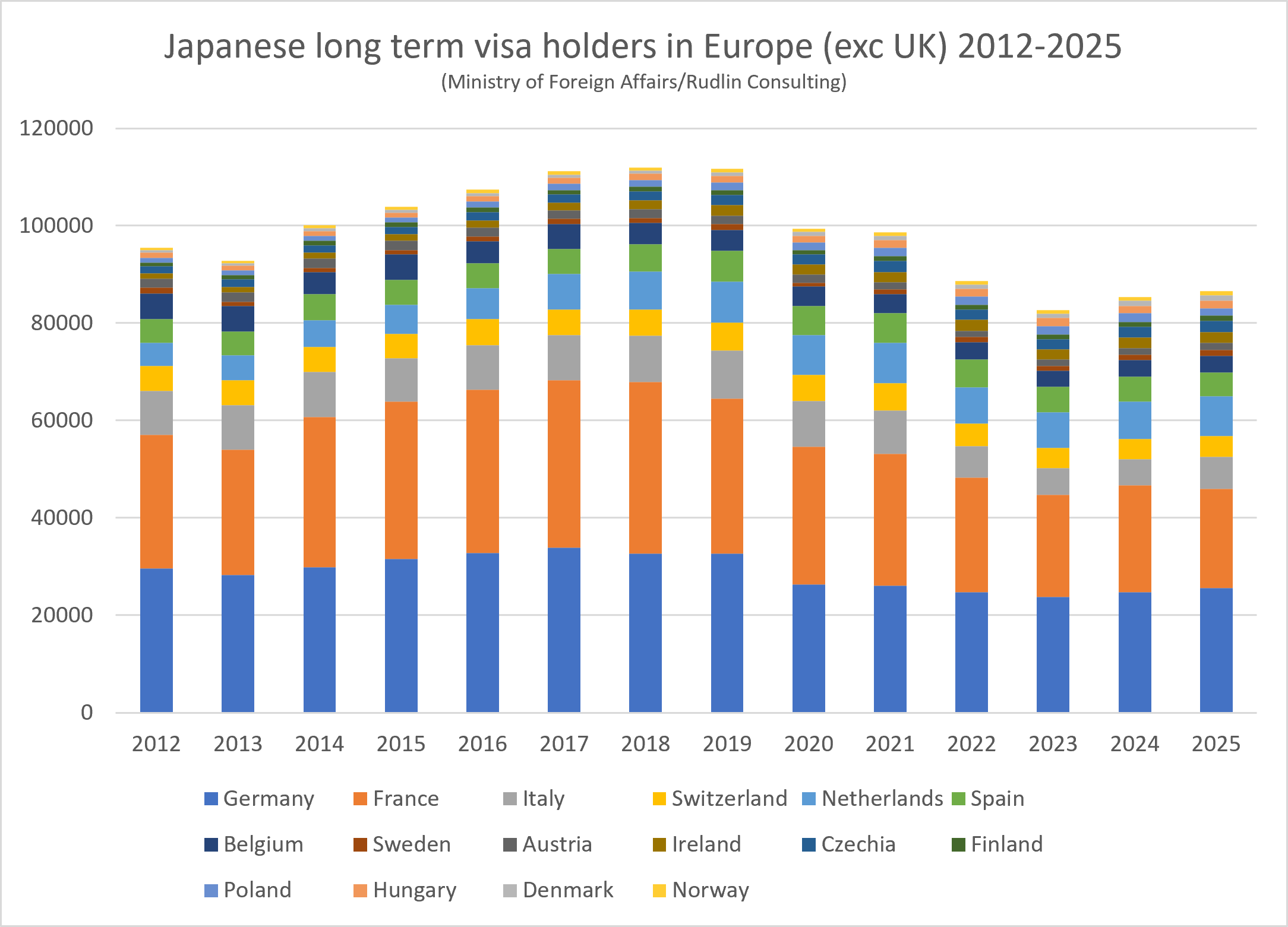

For other European countries, however, the number of long term visa holders stayed stable or even grew 2015-2019 in Europe overall. Again, there was a drop during the pandemic, but some signs of recovery 2023-2025.

Figure 6. Japanese long-term visa holders in Europe (excluding the UK), 2012–2025.

Corporate expatriates vs student and academic visas

To analyse this difference between European countries further, we need to look at the two largest categories for long term visa holders – corporate expatriates and student and academic visas.

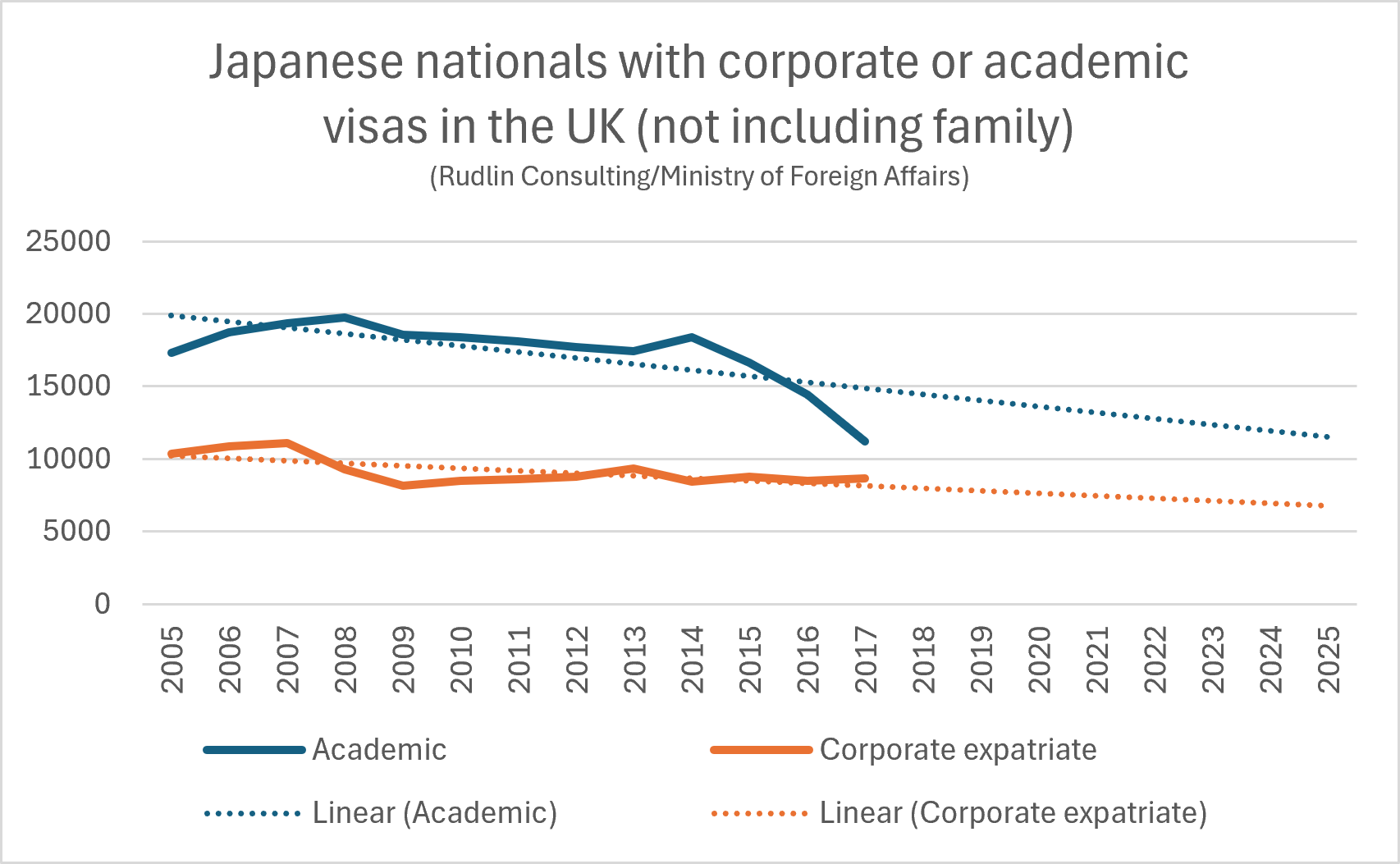

Unfortunately the Japanese Ministry of Foreign Affairs data only shows these categories by country for 2005 to 2017. We have added in a trend line for the UK charts below, and as can be seen, there was a significant drop in the number of academic visas from 2015 (preceded by a sudden rise the year before) and after a decline around the time of the Lehman Shock, corporate expatriate visas remained fairly steady to 2017.

The UK had been the second largest host of Japanese nationals with academic, research or student visas in 2011, after the USA. It lost the number two spot to Australia over the 2015 to 2017 period, when visa holders in that category in the UK fell by a third – from 16,636 to 11,189 (not including dependants). The UK was the only country out of the major hosts of academic visas to experience such a major decline in Japanese student numbers. Canada was not far behind the UK in 2017 and may well have overtaken it in the years after. France and Germany held steady.

Figure 7. Japanese nationals in the UK on corporate or academic visas (excluding family), 2005–2017, with trend lines.

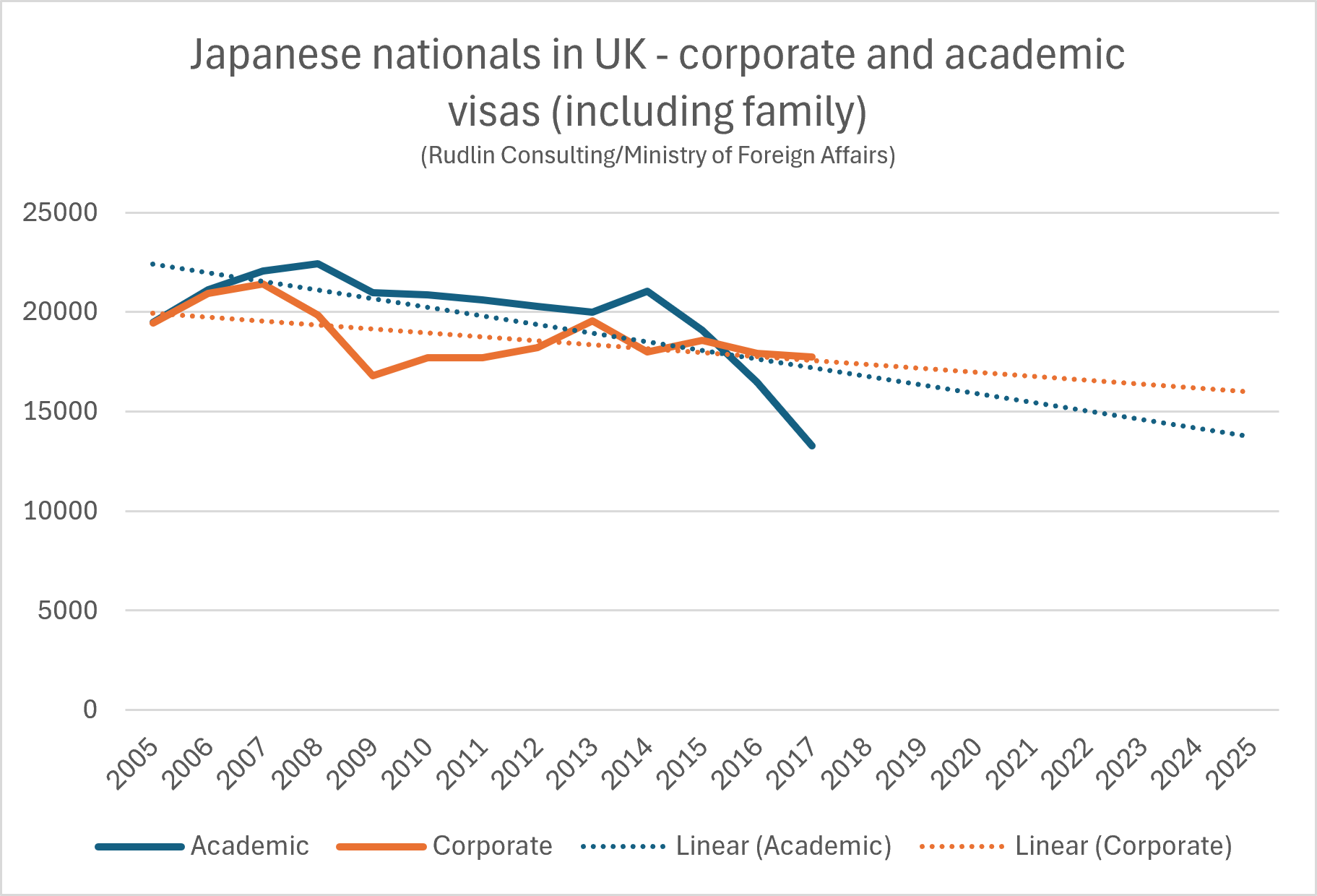

If we add in the dependents and family they bring with them, then the picture looks like this:

Figure 8. The same categories including accompanying family.

The gender balance and dependants

One point to note is that around 66% of those Japanese nationals on academic or student visas were female in 2005 and 64% in 2017. 21% of those on corporate expatriate visas were female in 2005 and 26% in 2017.

There was only one dependant for every eight student or academic visa holders in 2005, and around one dependant for every five student/academic visa holders in 2017. This was significantly lower than for other nationals such as students from Nigeria (more than one dependant per student) or India – around 1 dependant for every three students. Whereas there was around one dependant per Japanese corporate expatriate visa holder throughout the same period.

It is also worth noting that around 70% of the dependants of corporate expatriates were female, reflecting the traditional pattern of the wife being the trailing spouse – or if the woman was herself on a corporate expatriate visa, being a younger, single woman.

For the academic and student visas, around 60% of the dependants were female, again perhaps reflecting that women students and academics tend to be single, whereas the male academics and students are often accompanied by their female partners and children. This may well have fed into the rise in Japanese permanent residents – single women coming to the UK to study, meeting a romantic partner and deciding to settle in the UK.

So what happened around 2015 to impact Japanese student, researcher and academic visa holders in the UK?

The changes to student visas introduced in 2015 would have had a strong negative impact on Japanese students who were looking to join English language school courses, foundation years or A-level or pathway programmes, as a Secure English Language Test was introduced – which had to be taken at a UK Visas and Immigration-approved test centre. There were only two such centres in Japan – in Tokyo and Osaka. Biometric identification was also required. Ordinary IELTS tests taken outside a UKVI-approved centre were no longer accepted for visa purposes; only the ‘IELTS for UKVI’ test counted.

The British Council’s research and JASSO analysis subsequently pointed to these changes as a contributing factor to the roughly 13% fall in Japanese exchange students to the UK between 2015/16 and 2016/17, a drop that the US and Australia — which did not impose equivalent restrictions — did not experience.

There was a transitional window, which might explain the upward blip in visas obtained in 2014 – to avoid the new regulations in 2015.

For degree level students there were no changes to the previous regime but the financial requirements were tightened. Students were required to demonstrate they held sufficient maintenance funds — tuition fees plus £1,020/month for London or £820/month elsewhere (for up to 9 months), held continuously for 28 days before the visa application. The abolition of the “established presence” provision meant students who had been in the UK for some time could no longer use a more relaxed evidential standard; everyone had to show the full funds upfront.

This would have impacted the Japanese nationals who had come over with their parents on a corporate expatriate visa, gone through the British education system and now wanted to study at a British university. A child of a Japanese and British parents can have dual nationality until they are 20, but would have to choose which one to keep at that point. Given the expense of international student fees, this may have motivated some of them to register with UK universities as a domestic British student.

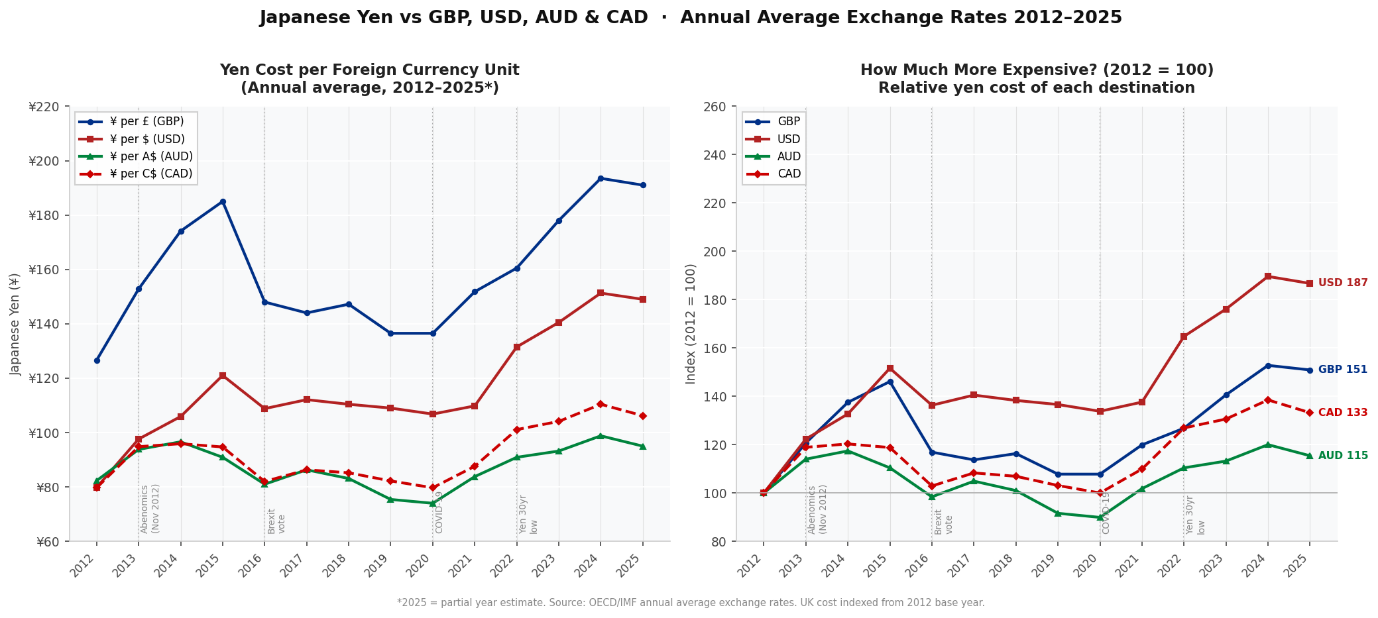

To add to the financial requirements, the Japanese yen had been weakening and approached ¥195 to the £ in 2015. It then strengthened against the £ in 2016-2020, but has since weakened again. It is notable that the yen did not weaken as much against the Canadian or Australian dollar.

Figure 9. The yen against the pound, dollar, Australian and Canadian dollars, 2012–2025 (annual averages; right-hand panel indexed to 2012 = 100).

It seems highly likely then that the number of students who were Japanese nationals on degree courses of over a year declined due to financial issues, and the number of students who were Japanese nationals on shorter courses declined due to student visa regulations tightening – or that those students may have switched to a standard visitor visa instead. Many students went to cheaper countries and courses.

What explains the decline in corporate expatriates?

While corporate expatriate numbers held steady from 2015 to 2017 at around 8,500 (principals only, not including dependants) or so, over the 2005 to 2017 period there was a 16% decline – compared to the 35% decline for academic and student visas – which mainly related to the 2015-2017 period. The peak for Japanese corporate expatriates in the UK was in 2007, at 11,000, dropping to 9,200 in 2008 and to 8,151 in 2009, then holding steady to 2017. It seems likely then that the first event to have a negative impact on Japanese corporate expatriation to the UK was the Global Financial Crisis of 2007-9.

As noted above, the publicly available Ministry of Foreign Affairs data stopped splitting long term visa holders into corporate and student/academic categories from 2017. It is hard therefore to estimate to what extent the steady decline in long term visa holders in the UK since 2019 was due to fewer Japanese corporate expatriates.

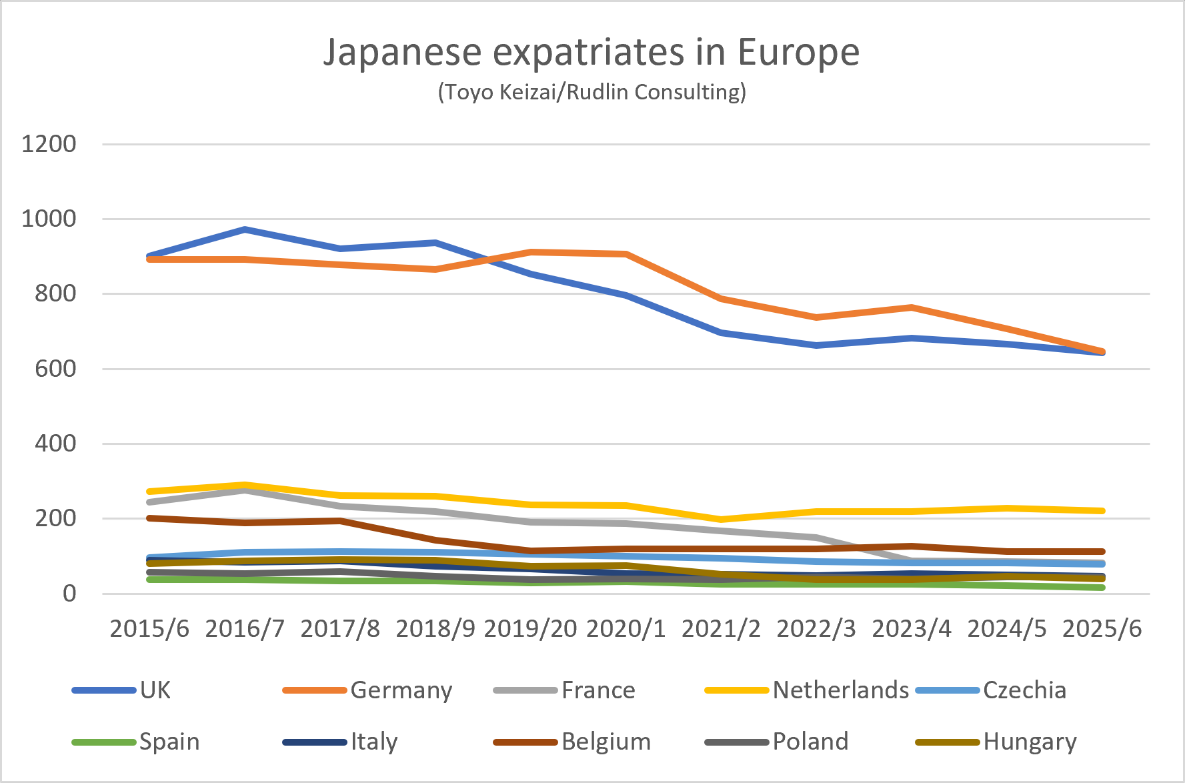

A further data source on Japanese corporate expatriates is the annual directory issued by Toyo Keizai. Their data gathering is reliant on companies completing their annual survey, so only shows part of the picture, but the response rate seems to be fairly consistent over the years, so may at least indicate the overall trends.

There was a decline of around a third across the main European hosts of Japanese nationals from 2015/6 to 2025/6. Germany (28% decline) overtook the UK (29% decline) as the top host in 2019/20 but is converging with the UK again. The decline in expatriate numbers was less steep in the Netherlands and Czechia and significantly higher than average in France, Spain, Hungary, Italy, Belgium.

Figure 10. Japanese expatriates in Europe, 2015/16–2025/26 (Toyo Keizai / Rudlin Consulting).

This seems to indicate that the impact of Brexit on the UK in terms of Japanese expatriates was in the context of an overall decline in Japanese expatriates to Europe, and the UK fared quite well. Our hunch is that the UK continued to be an important host for Japanese financial services sector companies and trading companies – who tend to have a large proportion of Japanese expatriates. The Netherlands fared better after Brexit due to the transfer of logistics and European functional hubs to the Netherlands, and Czechia probably attracted expatriates in the automotive sector.

In conclusion, there were three key factors impacting Japanese corporate expatriate presence:

Access to the EU market – the Netherlands, which combines EU membership with an English-speaking business environment, doubled its Japanese long-term population over the decade 2015-2025.

The cost of moving staff – the immigration costs for working visas to the UK rose sharply just as the yen weakened: the Immigration Health Surcharge rose 66% in February 2024 to £1,035 per person per year, the Immigration Skills Charge rose 32% in December 2025 to £1,320 per year for large sponsors, and the combined upfront cost of a five-year UK Skilled Worker visa (around £12,500) has been estimated at roughly ten times the average of comparable countries.

For a typical Japanese expatriate with a spouse and two children on a five-year posting, upfront immigration costs alone now exceed £30,000 – a real consideration when Tokyo HQ compares London with Amsterdam or Düsseldorf.

The final factor is economic growth. Japanese multinationals are in search of growth overseas, to compensate for their ageing, declining population at home. The UK is currently in a chicken and egg situation. Japanese foreign direct investment can help the UK to grow, but it needs to be assured that the UK is indeed a growth market.

Implications for policy makers

In the interests of attracting further investment from Japan, some kind of special arrangement could be made for reducing the costs of intra-company transfer visas. Any positive impact of this, however, would be dampened by the UK being outside the EU for market access, the overall decline in Japanese corporate expatriation and the UK’s attractiveness in terms of economic growth relative to other European countries and other regions. The major Japanese companies are already in the UK and unlikely to leave – but also unlikely to expand greatly regardless of incentives. The most likely newcomers will be the small to medium size Japanese companies, possibly more recently established and in new, emerging sectors.

The number of Japanese international students in the UK has always been relatively small compared to those of other nationalities, so it is unlikely that any move to encourage more Japanese students will be particularly controversial in terms of impacting immigration totals significantly. The Japanese government has announced that it is keen to encourage more Japanese students to study abroad, so would be open to such a proposal – and indeed agreements on Japanese scientific researchers transferring to the UK have already been signed. The weak yen is a major factor, however, which is out of the UK government’s control. There is pressure on the Japanese government to provide more funding for Japanese students to go abroad, to mitigate this.

Implications for suppliers to Japanese companies

The localization of Japanese companies’ senior management implies that the local decision makers and budget holders are increasingly locally hired Europeans or locally hired Japanese nationals with permanent residency. It may still be the case, however, that the final decision rests in Japan. In which case, having a presence in Japan, or making regular trips to there, will also be necessary part of the sales relationship.

For a sector by sector analysis of Japanese companies and their employees and the impact of M&A in the UK and Europe over the past 10 years, please see our next report.

© Rudlin Consulting Ltd 2026 · Source data: Japanese Ministry of Foreign Affairs (Annual Report of Statistics on Japanese Nationals Overseas) and Toyo Keizai, consolidated by Rudlin Consulting.