Is “chutzpah” in Israel the same as “not reading the air” in Japan?

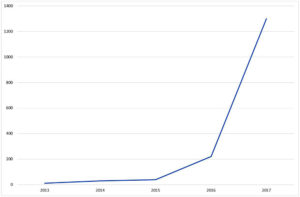

Japanese investment in Israel has shot up the past five years. According to JETRO there are 66 Japanese companies based in Israel as of 2017, 16% up on the previous year. Nikkei Business estimates the total of investment asY130bn (around $1.1bn) – the main contributor being Mitsubishi Tanabe Pharma’s acquisiton of Neuroderm for $1.1bn in 2017.

PM Abe’s visit to Israel in 2015 brought about many further visits from Japanese business people. The attraction is, unsurprisingly, Israel’s expertise in IoT, AI, cyber security and other technologies. But the big obstacle, certainly according to many people I have spoken to about this, is the big cultural communication gap.

According to Shintaro Hirado, who has set up a business support company in Israel, it can be seen as a positive, that Israelis are very straight with you, and once you get over the shock of that, then you can build good trusting relationships.

Japanese expatriates in Israel compare “Chutzpah” (cheek, nerve, audacity) to the KY (Kuuki Yomenai) phenomenon in Japan of a few years ago, when younger Japanese were accused of not being able to “read the air” (usually of disapproval).

Israeli owners of companies acquired by Japanese companies such as Rakuten have asked for earn outs before the final agreement was signed, or left due diligence meetings days before they were over, not out of anger, but just “I’ve said all I need to say.”

Japan Intercultural Consulting – whom Rudlin Consulting represents in Europe, Middle East & Africa – has just started a partnership with Charis Intercultural Consulting, who have a presence in Israel, so this communication gap could be a business opportunity for us too.

For more content like this, subscribe to the free Rudlin Consulting Newsletter. 最新の在欧日系企業の状況については無料の月刊Rudlin Consulting ニューズレターにご登録ください。

rudlin

rudlin rudlinconsulting

rudlinconsulting