Toridoll expands restaurant business further in Europe

Tokyo listed food company Toridoll Holdings (owner of Marugame Udon + Wok to Walk) has acquired The Real Greek + Franco Manca owner Fulham Shore for £93 million. It acquired 40% of UK based Shoryu Ramen in 2016 and Netherlands based Wok to Walk in 2015.

Marugame Udon Europe’s headquarters is in the UK, employing around 100 people, with 11 restaurants. It has plans to open 150 restaurant outlets across Europe by 2027, creating 10,000 jobs.

Marugame Udon had 7 restaurants in Russia, operating as franchises, but these seem to have disappeared from its network.

Wok to Walk has restaurants in 12 European countries.

For more content like this, subscribe to the free Rudlin Consulting Newsletter. 最新の在欧日系企業の状況については無料の月刊Rudlin Consulting ニューズレターにご登録ください。

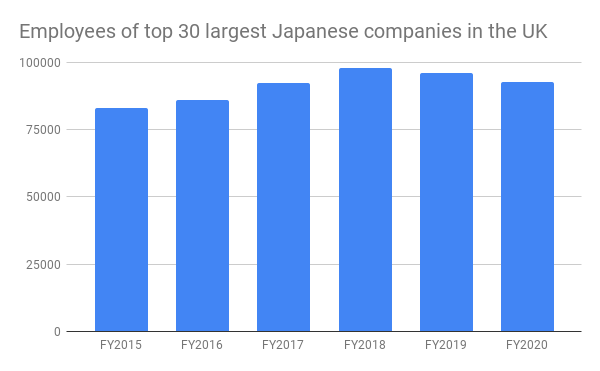

The total number of UK employees of the top 30 Japanese company groups fell 2.6% from 2019/20 to 2020/2021 – a strengthening of the downward trend in employee numbers since 2018/9. The peak of employment by the 30 largest Japanese company groupings in the UK was 97,827 in 2018/9 and this has now fallen by 5,000 to 92,851 employees. The top 30 represent around two thirds of the 137,000 people employed by 1,200+ Japanese companies in the UK.

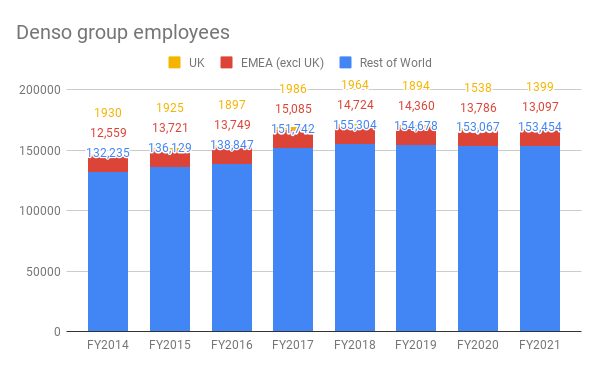

The total number of UK employees of the top 30 Japanese company groups fell 2.6% from 2019/20 to 2020/2021 – a strengthening of the downward trend in employee numbers since 2018/9. The peak of employment by the 30 largest Japanese company groupings in the UK was 97,827 in 2018/9 and this has now fallen by 5,000 to 92,851 employees. The top 30 represent around two thirds of the 137,000 people employed by 1,200+ Japanese companies in the UK. Konica Minolta acquired various UK companies before Brexit, but since Brexit has shrunk down and consolidated its operations in the UK and is focusing more on their European HQ in Germany and also the Czech Republic. The longer term trend of shifting away from manufacturing in the UK, to manufacturing elsewhere in Europe is seen at Denso, the Toyota group automotive parts manufacturer – UK employee numbers peaked in FY2018, and have been falling since, and are now 27.5% below the FY2014 level, whereas employment in the rest of the region is up 4.3% and global employee numbers, excluding UK, have risen 16% since FY2014.

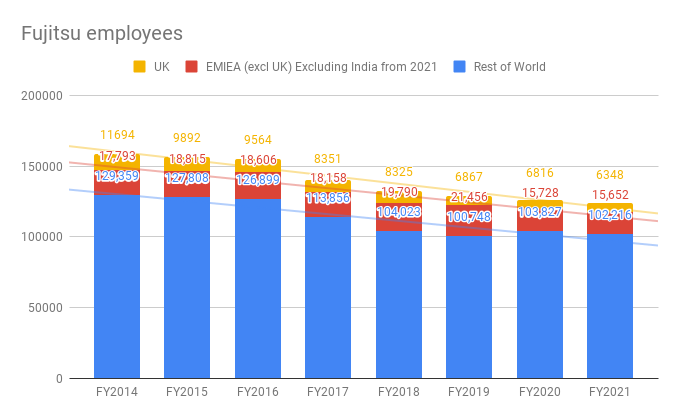

Konica Minolta acquired various UK companies before Brexit, but since Brexit has shrunk down and consolidated its operations in the UK and is focusing more on their European HQ in Germany and also the Czech Republic. The longer term trend of shifting away from manufacturing in the UK, to manufacturing elsewhere in Europe is seen at Denso, the Toyota group automotive parts manufacturer – UK employee numbers peaked in FY2018, and have been falling since, and are now 27.5% below the FY2014 level, whereas employment in the rest of the region is up 4.3% and global employee numbers, excluding UK, have risen 16% since FY2014. Five years’ ago, Fujitsu was the largest Japanese corporate group in the UK, with 9,892 people. It has lost 3,000 employees since, and was the fourth largest Japanese group in the UK in FY2020. As of FY2021, Fujitsu has 6,348 employees in the UK, 45% down on FY2016, compared to a 21% decrease globally, excluding the UK. Growth at Fujitsu has been in India (and Fujitsu’s CTO is Indian) and in its global delivery centres in countries such as Poland and the Philippines.

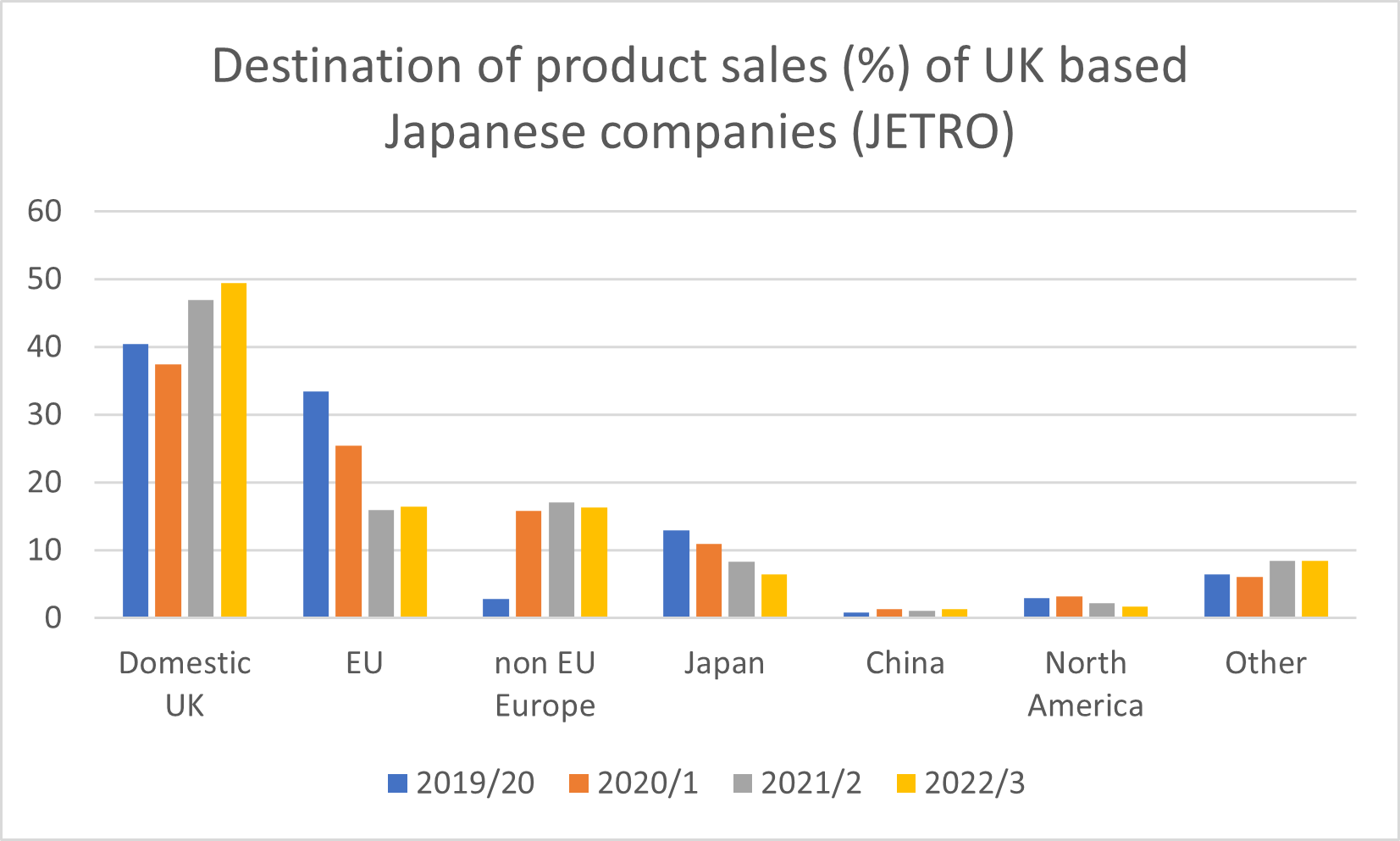

Five years’ ago, Fujitsu was the largest Japanese corporate group in the UK, with 9,892 people. It has lost 3,000 employees since, and was the fourth largest Japanese group in the UK in FY2020. As of FY2021, Fujitsu has 6,348 employees in the UK, 45% down on FY2016, compared to a 21% decrease globally, excluding the UK. Growth at Fujitsu has been in India (and Fujitsu’s CTO is Indian) and in its global delivery centres in countries such as Poland and the Philippines. Japanese companies in the UK are showing an increasing focus on the UK domestic market for their sales, with an average of 49.4% of sales to the UK market, 2.4% up on 2021/2, compared to a European average of domestic sales of 37.7%. UK companies are selling on average 16.5% of sales to EU countries, compared to 37.6% of sales to other EU countries (excluding their own country) for Japanese companies located in the EU. Unsurprisingly, Japanese companies in the UK have become more UK oriented since Brexit, as many of the EU sales and coordination functions have shifted from the UK to the EU – and is now potentially stabilising after the sharp decline over 2019/20 to 2021/2

Japanese companies in the UK are showing an increasing focus on the UK domestic market for their sales, with an average of 49.4% of sales to the UK market, 2.4% up on 2021/2, compared to a European average of domestic sales of 37.7%. UK companies are selling on average 16.5% of sales to EU countries, compared to 37.6% of sales to other EU countries (excluding their own country) for Japanese companies located in the EU. Unsurprisingly, Japanese companies in the UK have become more UK oriented since Brexit, as many of the EU sales and coordination functions have shifted from the UK to the EU – and is now potentially stabilising after the sharp decline over 2019/20 to 2021/2