LinkedIn

LinkedIn YouTube

YouTubeGMO Internet to close GMO-Z.COM London forex brokerage

Japan’s GMO Internet group was to sell off its GMO-Z.COM London based forex brokerage to Australia’s Invast Global as of October 2022. However, the Financial Conduct Authority did not approve the transfer of shares in March 2023 so Invast has cancelled the transaction. GMO Internet has disclosed in the latest annual report of GMO-Z.COM that it now intends to close the operation within the year. GMO-Z.COM was established in London in 2012 and employed 10 people, 17 at its peak in 2019. It was trying to shift from individual client services to institutional client services.

For more content like this, subscribe to the free Rudlin Consulting Newsletter. 最新の在欧日系企業の状況については無料の月刊Rudlin Consulting ニューズレターにご登録ください。

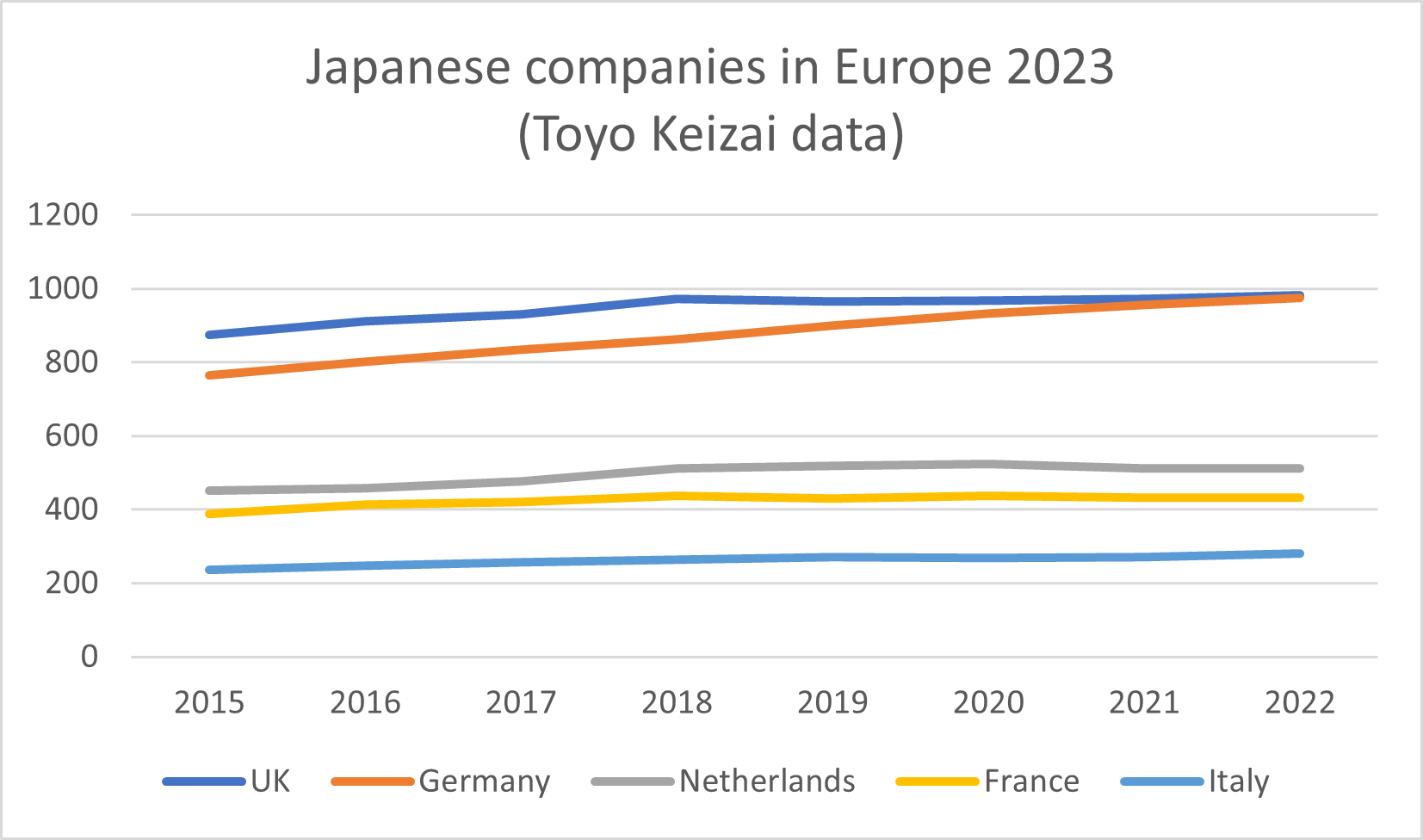

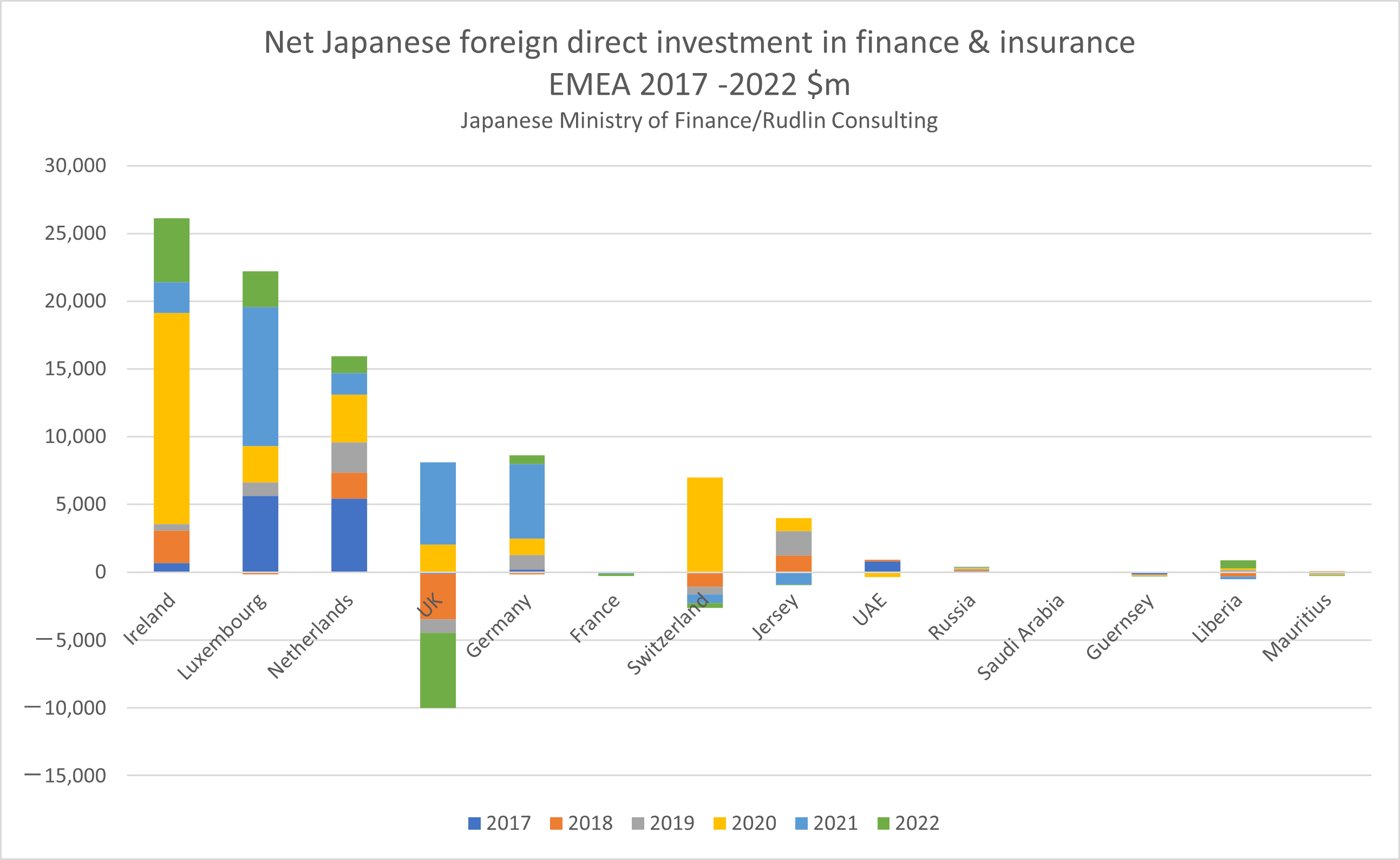

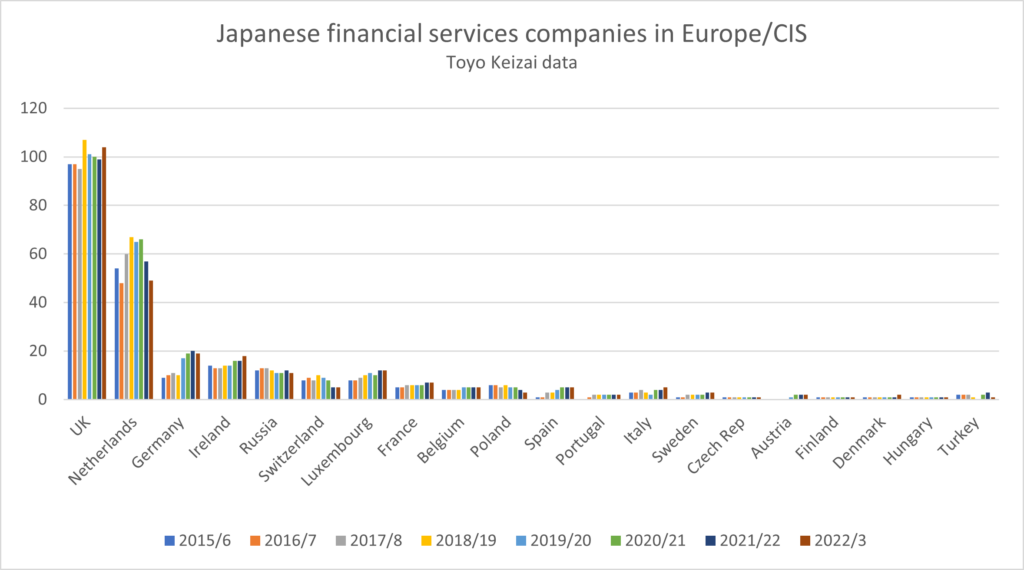

The other issue raised by the two pieces of research are whether other EU cities have benefited from any additional growth, which the UK has missed out on. As can be seen from the chart, Toyo Keizai data shows that there was an overall upward trend in the number of Japanese financial services companies in the European region, of around 12% from 2015/6 to 2022/23. The UK still dominates as a host, and the numbers of companies hosted rose 7% – so below trend. Germany doubled the number of Japanese financial services companies it hosted over the period. The numbers rose sharply in the Netherlands and then dropped. Just as Dr Hall’s research suggests, Ireland, Luxembourg and France seem to have benefited, albeit from a much smaller base.

The other issue raised by the two pieces of research are whether other EU cities have benefited from any additional growth, which the UK has missed out on. As can be seen from the chart, Toyo Keizai data shows that there was an overall upward trend in the number of Japanese financial services companies in the European region, of around 12% from 2015/6 to 2022/23. The UK still dominates as a host, and the numbers of companies hosted rose 7% – so below trend. Germany doubled the number of Japanese financial services companies it hosted over the period. The numbers rose sharply in the Netherlands and then dropped. Just as Dr Hall’s research suggests, Ireland, Luxembourg and France seem to have benefited, albeit from a much smaller base.