LinkedIn

LinkedIn YouTube

YouTubeTop 30 Japanese Employers in Italy 2022

The 30 largest Japanese company groups in Italy employ around 30,000 people across 85 companies in 2022, a 4% increase on 2021. This represents around two-thirds of the total number employed by Japanese companies in Italy.

Some of this growth was driven by acquisition – for example the Hitachi group of companies (the second largest Japanese employer in Italy) now includes Hitachi Energy, as a result of Hitachi’s acquisition of ABB’s power grids business. Yamaha Motor has also acquired Motori Minarelli.

The workforce of the largest Japanese employer in Italy, the NTT group of companies, has grown organically by 5.75% and Toyota Industries/Toyota Material Handling also has grown substantially.

Automotive related companies such as Denso, AGC and NSG (the latter two making automotive glass) have shrunk slightly but tyre manufacturer Bridgestone has grown. Other manufacturers such as Princes (foods company owned by Mitsubishi Corporation) and Ebara Pumps have cut back their workforce.

The top 30 company groups can be downloaded for free below. We can provide more detail on the 85 companies within the Top 30 – each company name in full and employee total per company (a truer indicator of size of the company than turnover in our opinion) for £9.99 – please email us for a PayPal invoice.

DOWNLOAD FREE PDF OF TOP 30 LARGEST JAPANESE EMPLOYERS IN ITALY

For more content like this, subscribe to the free Rudlin Consulting Newsletter. 最新の在欧日系企業の状況については無料の月刊Rudlin Consulting ニューズレターにご登録ください。

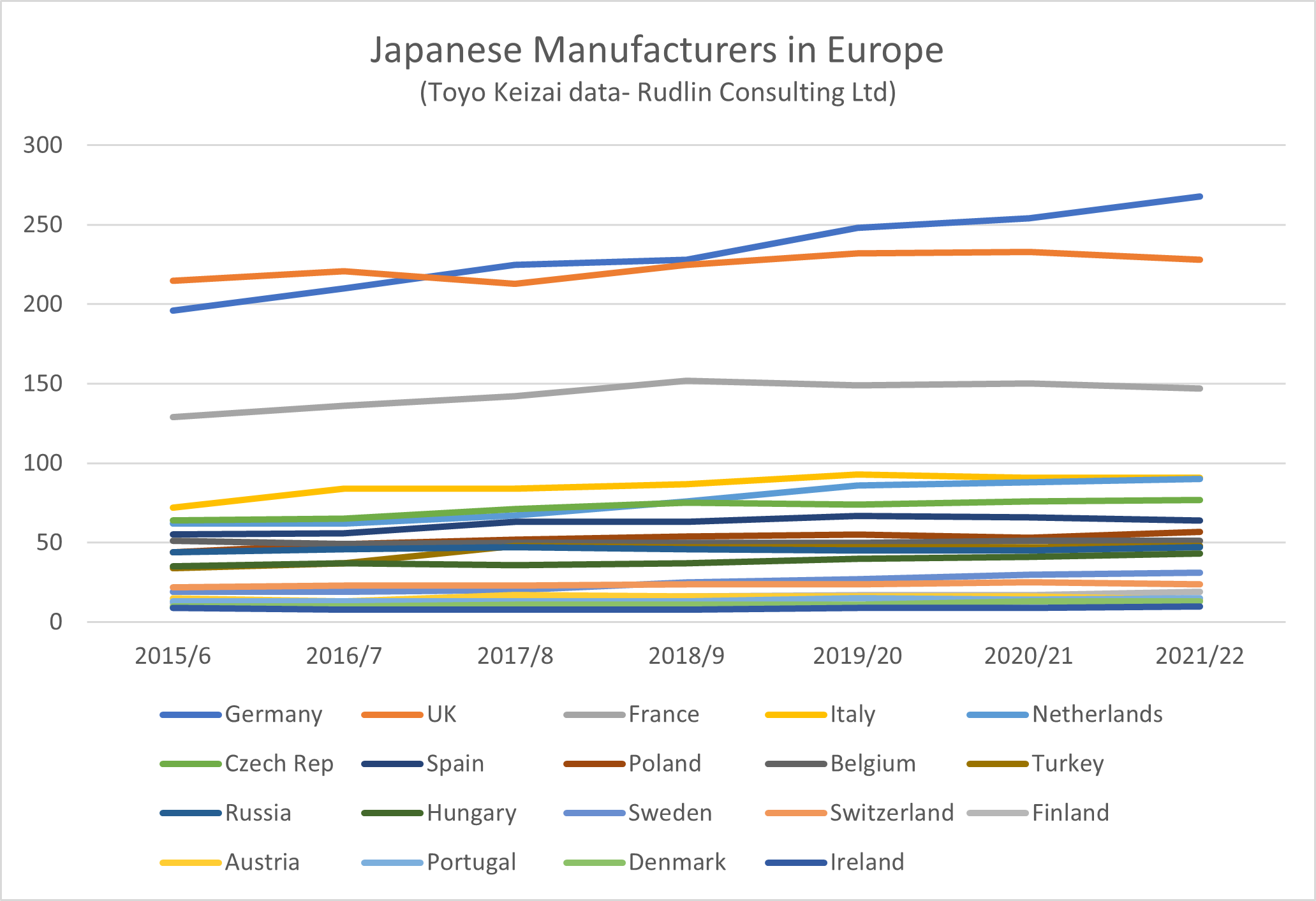

How this compares with other European countries can be seen in the chart on the left – which shows the numbers of all manufacturing companies in Europe, including automotive. According to Toyo Keizai, the number of Japanese manufacturers in the UK dipped around 2017/8, but recovered, with another more recent fall. But there was growth overall since 2015/6, with 228 companies in 2021/2 compared to 215 in 2015/6 – a 6% increase. This is much lower than the overall 20% growth in Europe, and as a consequence the UK is no longer the largest host of Japanese manufacturers.

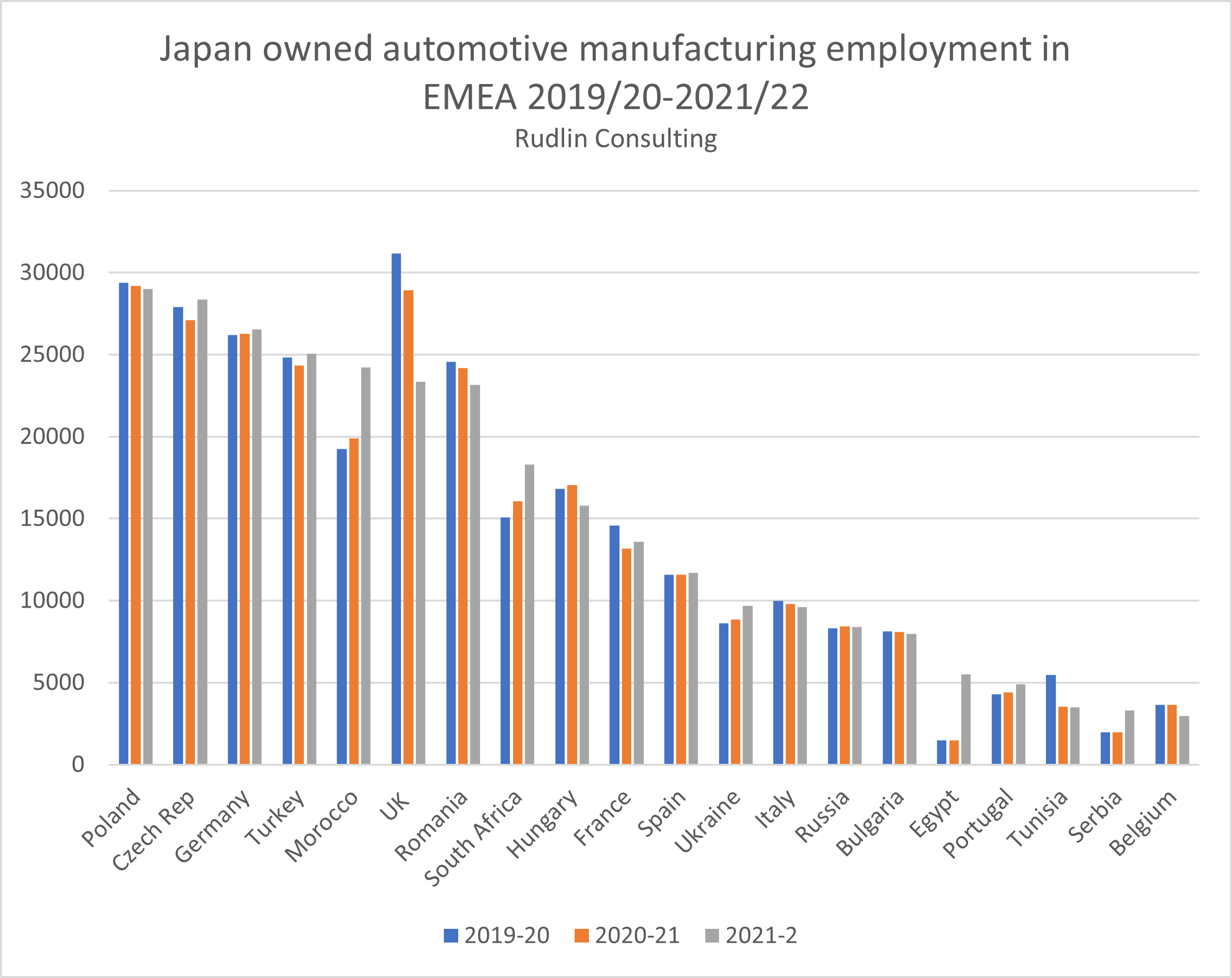

How this compares with other European countries can be seen in the chart on the left – which shows the numbers of all manufacturing companies in Europe, including automotive. According to Toyo Keizai, the number of Japanese manufacturers in the UK dipped around 2017/8, but recovered, with another more recent fall. But there was growth overall since 2015/6, with 228 companies in 2021/2 compared to 215 in 2015/6 – a 6% increase. This is much lower than the overall 20% growth in Europe, and as a consequence the UK is no longer the largest host of Japanese manufacturers. numbers of Japanese automotive manufacturing employees in the EMEA region. According to our estimates, the UK will slip to 6th position in 2021-2022, due to the closure of Honda‘s Swindon plant, along with many of its suppliers shutting down operations. It will be overtaken by Czech Republic, Germany, Turkey and Morocco.

numbers of Japanese automotive manufacturing employees in the EMEA region. According to our estimates, the UK will slip to 6th position in 2021-2022, due to the closure of Honda‘s Swindon plant, along with many of its suppliers shutting down operations. It will be overtaken by Czech Republic, Germany, Turkey and Morocco.

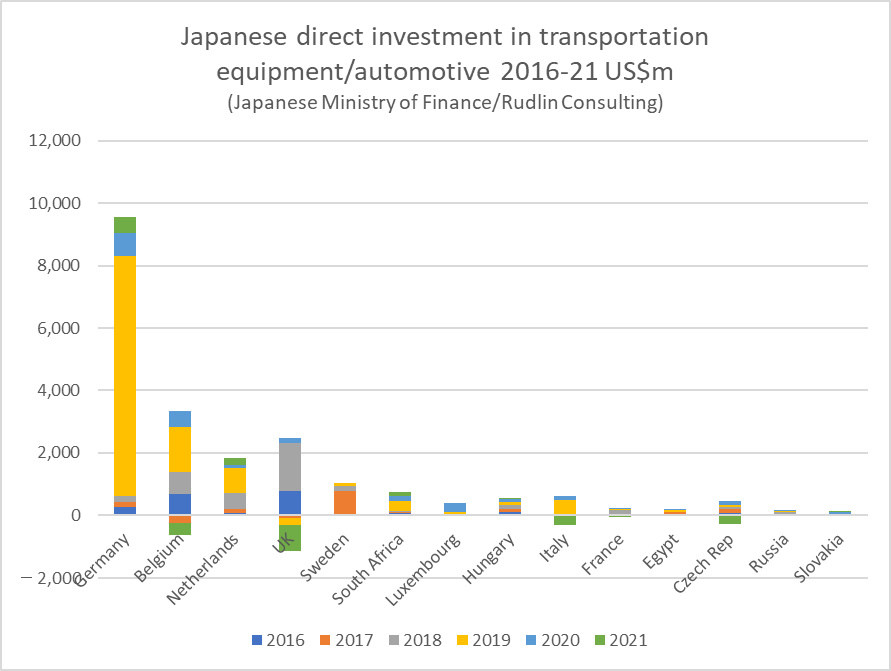

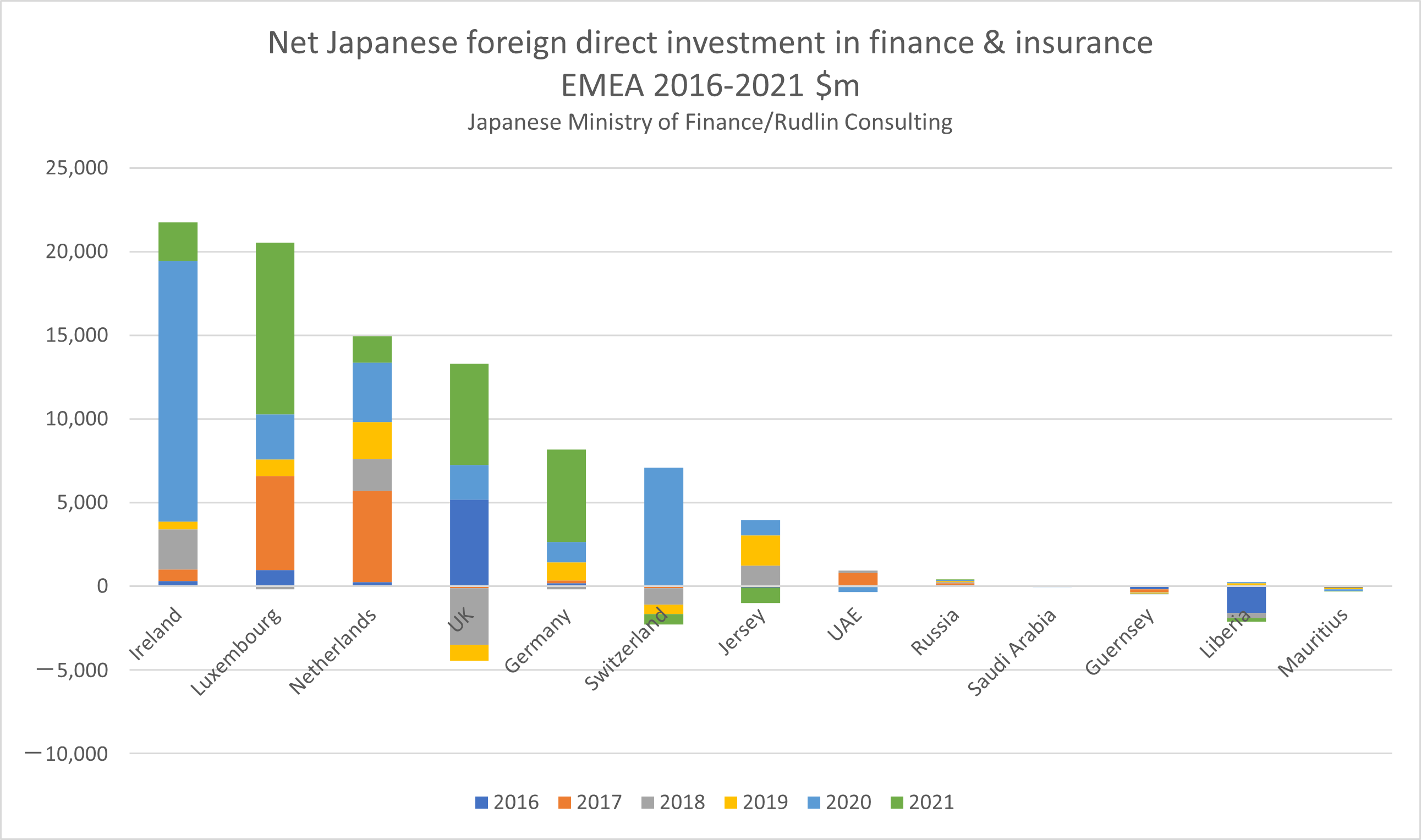

Examining the statistics from Japan’s Ministry of Finance on direct investment flows, it seems the UK benefitted from a big inward investment from Japan into the finance and insurance sector in 2016, then there was net disinvestment in 2017-2019, and then increasing net investment in 2020-21. Conversely, there was little investment into Ireland, Luxembourg or the Netherlands in 2016, but major investments into their finance and insurance sectors in 2017, 2018 and 2020-21.

Examining the statistics from Japan’s Ministry of Finance on direct investment flows, it seems the UK benefitted from a big inward investment from Japan into the finance and insurance sector in 2016, then there was net disinvestment in 2017-2019, and then increasing net investment in 2020-21. Conversely, there was little investment into Ireland, Luxembourg or the Netherlands in 2016, but major investments into their finance and insurance sectors in 2017, 2018 and 2020-21.